Longer-Term Exchange Rate Anchors

受取状況を読み込めませんでした

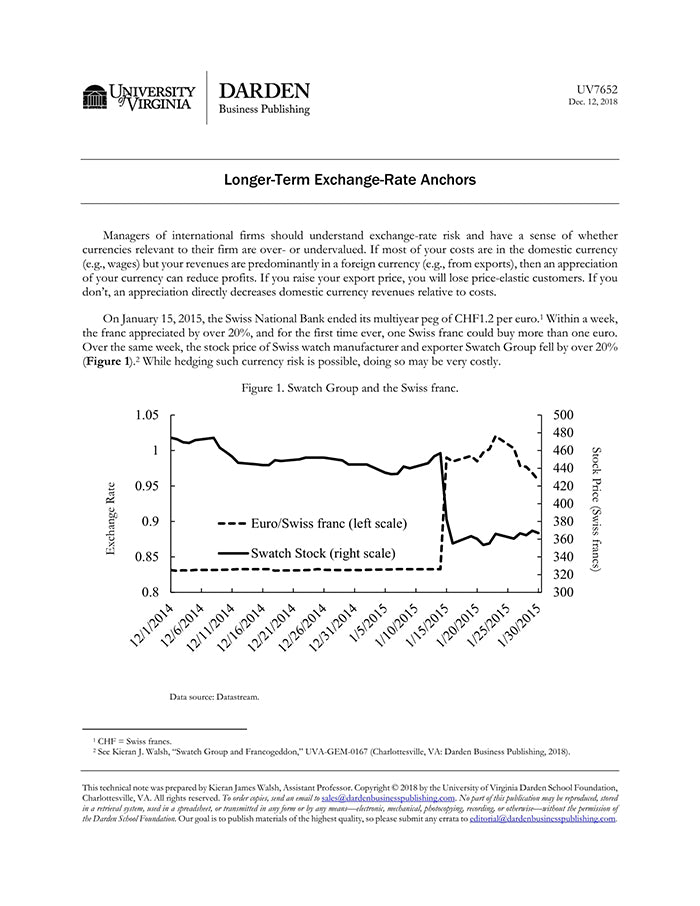

The goal of this technical note is to give students tools for thinking about how exchange rates will move over a period of five years into the future. While forecasting exchange rates is arguably more art than science, managers, policymakers, and investors are nonetheless often required to form opinions about the future evolution of exchange rates. Specifically, this note defines the real exchange rate and purchasing power parity (PPP) and illustrates that PPP is useful in forecasting nominal exchange rate movements for advanced economies (AEs). For emerging market economies (EMEs), the note explains that PPP is less useful and instead offers a relatively new International Monetary Fund (IMF) model, which evaluates exchange rate over- and undervaluation in EMEs (as well as AEs). The note is designed to be used in a first-year MBA course, specifically in a class structured around exchange-rate forecasts based on recent supplemental data (to be added by the instructor). In that case, the class would build from a question like, "What will the US dollar/British pound exchange rate be in five years, and why?" Note that the IMF material is advanced and, depending on the level of the students and place in the course, may need to be presented as a useful "black box." In any case, this note could also be employed in an advanced undergraduate or master's level course on international finance or macroeconomics.

【書誌情報】

ページ数:12ページ

サイズ:A4

商品番号:HBSP-UV7652

発行日:2018/12/12

登録日:2019/1/29